Britain saw the biggest tax hike on workers among advanced economies last year, according to new data from the Organisation for Economic Co-operation and Development (OECD). The UK’s “tax wedge” rose by 2.45 percentage points in 2025 — the largest increase across the OECD’s 38 member countries.

Understanding the tax wedge

The tax wedge is a measure of the total tax burden on labour. The OECD defines it as the sum of personal income tax, employee and employer social security contributions, and any payroll taxes, minus any cash benefits received by the employee. This total is expressed as a percentage of the employer’s total labour costs. In plain terms, it captures the difference between what it costs an employer to hire a worker and what that worker actually takes home in net pay. The higher the tax wedge, the greater the proportion of labour costs that goes to tax rather than the employee’s pocket.

Despite the sharp rise, the UK’s overall tax wedge of 32.4 per cent remained below the OECD average of 35.1 per cent. The range across member states is vast: from zero in Colombia to 52.5 per cent in Belgium.

OECD data: UK leads in tax wedge growth

Among the 38 OECD countries, 24 saw their tax wedge increase in 2025, while 11 recorded a decline and three remained unchanged. The UK’s 2.45 percentage-point rise was the highest. Estonia posted the second-largest increase at 1.95 percentage points, followed by Germany at 1.34 and Israel at 1.09. No other nation recorded an increase above one percentage point.

Drivers of the increase

The OECD attributed the rise to measures introduced by Chancellor Rachel Reeves in the October 2024 Budget, notably increases to employer National Insurance contributions (NICs). The employer NIC rate rose from 13.8 per cent to 15 per cent from April 2025, and the secondary threshold — the point at which employers start paying NICs — was cut from £9,100 to £5,000 per year. The report also cited “fiscal drag” as a significant factor: because income tax thresholds are frozen, rising earnings push more people into higher tax brackets, increasing their effective tax rate.

The 2024 Budget introduced a total of approximately £40 billion in tax rises. These included increases to capital gains tax (the lower rate rising from 10 per cent to 18 per cent, the higher rate from 20 per cent to 24 per cent), reforms to inheritance tax (including subjecting inherited pension pots to inheritance tax from April 2027), a 20 per cent VAT charge on private school fees from January 2025, and the abolition of the non-domiciliary tax regime. The OECD’s methodology includes taxes paid by employers as well as those paid by employees, meaning that the rise in employer NICs is captured in the tax wedge even though it does not directly affect employees’ take-home pay.

Before the 2024 general election, Labour leader Keir Starmer pledged that his party would not raise taxes on working people. That commitment covered income tax, employee NICs and VAT. Employer NICs were not included in that pledge, and the OECD’s tax wedge calculation accounts for both sides of the employment relationship.

Government response

A Treasury spokesman defended the Budget measures, stating: “The decisions we made at the budget mean we can stabilise the economy and deliver support for families and businesses, including cutting the cost of living. Increasing the national minimum wage boosts pay for over 200,000 young workers, and employer national insurance contributions are lower when hiring under-21s.”

To mitigate the impact of higher employer NICs on small and medium-sized enterprises, the Employment Allowance was increased from £5,000 to £10,500, and the previous £100,000 eligibility threshold was removed.

Economic context and business impact

Business groups have raised concerns about the cumulative effect of higher employer NICs, alongside increases in the national minimum wage and planned employment reforms. Some employers have reportedly been considering redundancies to offset rising wage bills.

Recent labour market data shows that the UK unemployment rate stood at 4.9 per cent in the three months to February 2026, a decline from 5.2 per cent in the previous three-month period but still above the 4.2 per cent recorded before the 2024 election. Unemployment rose by 94,000 quarter-on-quarter to 1.883 million in the three months to December 2025, but the February 2026 figure marked the first quarterly decline in unemployment in approximately 20 months. The employment rate decreased slightly in the December-to-February period, while economic inactivity increased. Job vacancies have fallen to below pre-pandemic levels. Lower-paying sectors including hospitality, leisure and retail have experienced the largest reductions in employment. Young people aged 16 to 24 not in full-time education are now recording their lowest employment rate in a decade. Regional disparities are widening, with the North East and the West Midlands seeing the steepest falls in employment.

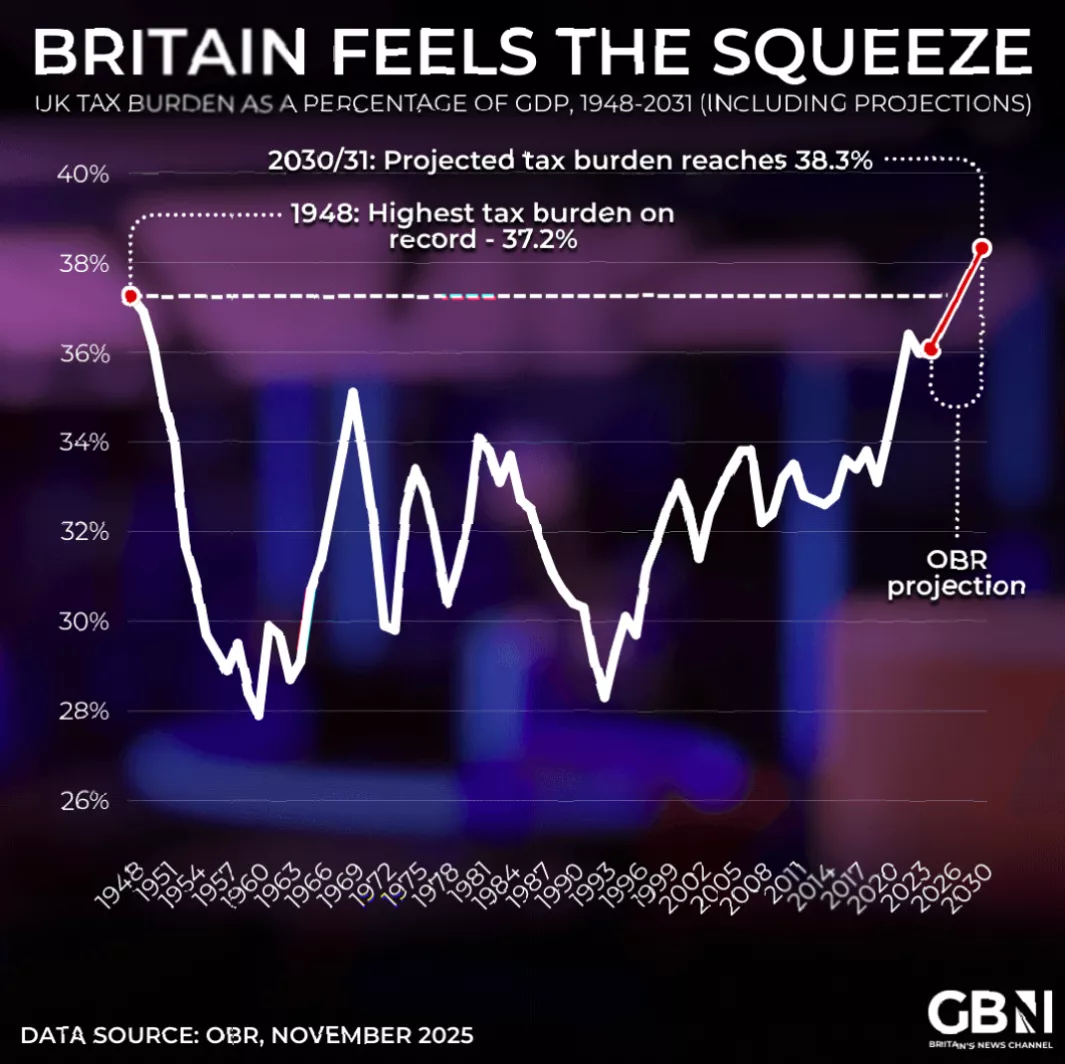

The International Monetary Fund (IMF) has warned that the UK’s overall tax burden as a share of gross domestic product is expected to rise faster than any other G7 country between 2024 and 2031, with projections reaching 42.1 per cent of GDP by 2031 — a level not seen since the Second World War. Economists have also highlighted risks linked to global pressures, including the economic impact of the ongoing conflict in Iran, which has disrupted oil and gas supplies, leading to price spikes, increased inflation and higher energy bills. The OECD has revised down its growth expectations for the UK in 2026 because of these global pressures, and poorer households are expected to be disproportionately affected.

The IMF has further advised against further pre-election tax cuts, suggesting tax rises may be necessary in the future. Concerns have been raised about whether the UK has reached a maximum sustainable level of taxation, with potential implications for work incentives and the motivation of individuals to remain in the country.