Ed Miliband’s potential succession to the leadership of the Labour Party is facing intense scrutiny, with his uncompromising stance on North Sea energy development emerging as the defining flashpoint. As the future of Sir Keir Starmer hangs in the balance, the Doncaster North MP – who previously led the party from September 2010 to May 2015 and was appointed Secretary of State for Energy Security and Net Zero when Labour returned to power in July 2024 – has been repeatedly named by Westminster commentators as a possible replacement. Yet the former leader’s record on domestic oil and gas, combined with his outright refusal to guarantee approvals for key North Sea projects, has reignited a fierce debate about the economic and security consequences of his approach.

Energy Policy Under Scrutiny

At the centre of the dispute is the fate of the Jackdaw gas field and the Rosebank oil field, two major developments that have been stalled by legal challenges and regulatory uncertainty. Production at Jackdaw had been scheduled to begin this year, while first output from Rosebank’s phase one was planned for 2026–2027. However, following a Supreme Court ruling on fossil fuel developments that required full consideration of scope 3 emissions – the emissions from burning the extracted fuel – the initial approvals were withdrawn. Under a Chancellor Miliband, the original wire article suggests, there seems no prospect of any North Sea development whatsoever, with even Jackdaw and Rosebank looking like they will be vetoed. When grilled on the issue by Sky News, Miliband refused to be drawn on whether he would allow the fields to go ahead, insisting only that the Government had “a proper planning process” and that he would “look at all of the facts” as a decision maker.

The research briefing provides further detail on the legal history. The Jackdaw gas field, operated by Shell, saw its consents ruled no longer valid by a Scottish court in January 2025, though work could continue pending a government consultation on scope 3 emissions. Shell had made a final investment decision in July 2022, and when operational the field is expected to contribute around 6.5% of UK Continental Shelf gas production, enough to heat over 1.4 million homes. The Rosebank oil field, described as the UK’s largest untapped oil field and located west of Shetland, was approved by the previous government in 2023 despite significant opposition. In January 2025 a legal challenge ruled that approval unlawful for failing to consider the full climate impact of burning the extracted oil and gas, forcing a fresh authorisation process. Rosebank is majority owned by Adura, a joint venture between Shell and Equinor, and an estimated 90% of its reserves are oil, with the majority intended for export. Environmental groups have argued that Rosebank will not deliver energy security or lower bills because most of its oil will be sold overseas.

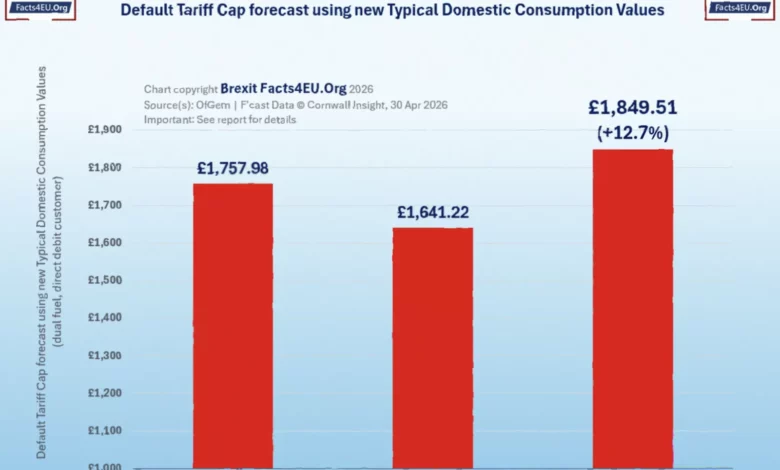

The implications for UK energy security extend well beyond these two projects. The original article states that there are no plans to secure UK security outside renewables, that suggestions of easing the tax burden for oil and gas companies will be given no consideration, and that any prospect of “de-linking” world prices from UK prices appears off the agenda. As a result, households will continue to be exposed to the volatility of global energy markets, described in the original piece as being at the “mercy of the Iran War” when it comes to bills. The lack of major tax revenues from home-grown oil and gas exploration will, in turn, impact the Chancellor’s ability to pay for any potential rising bills. The Energy Price Cap – a limit on what suppliers can charge domestic consumers per kilowatt hour, set quarterly by Ofgem – is currently £1,641 per year for a typical household paying by direct debit for the period April to June 2026, a 6.6% decrease partly due to the removal of green levies announced in the Autumn Budget of 2025. The cap applies to standard variable tariffs and is calculated using typical domestic consumption values of 2,700 kWh of electricity and 11,500 kWh of gas per year.

Former Conservative minister Lord Redwood has been among the most vocal critics, telling the original article that Miliband’s “largely unrestrained net zero policies” have led to the “disastrous closure of two oil refineries, just when we need their home-produced jet fuel.” He warned that the refusal to allow more domestic oil and gas leaves the UK short of necessities when the Gulf is closed and world deliveries are down, and that “sky-high energy taxes just drive away investment, jobs and business, leading to less overall tax collected as jobs and orders flee our shore.” Lord Redwood called for a prime minister and chancellor willing to “override net zero madness” and do deals with the oil, gas and refining industry to increase home production and improve security of supply, adding: “Importing everything that needs energy is self-harm on a huge scale.”

Broader Economic Concerns

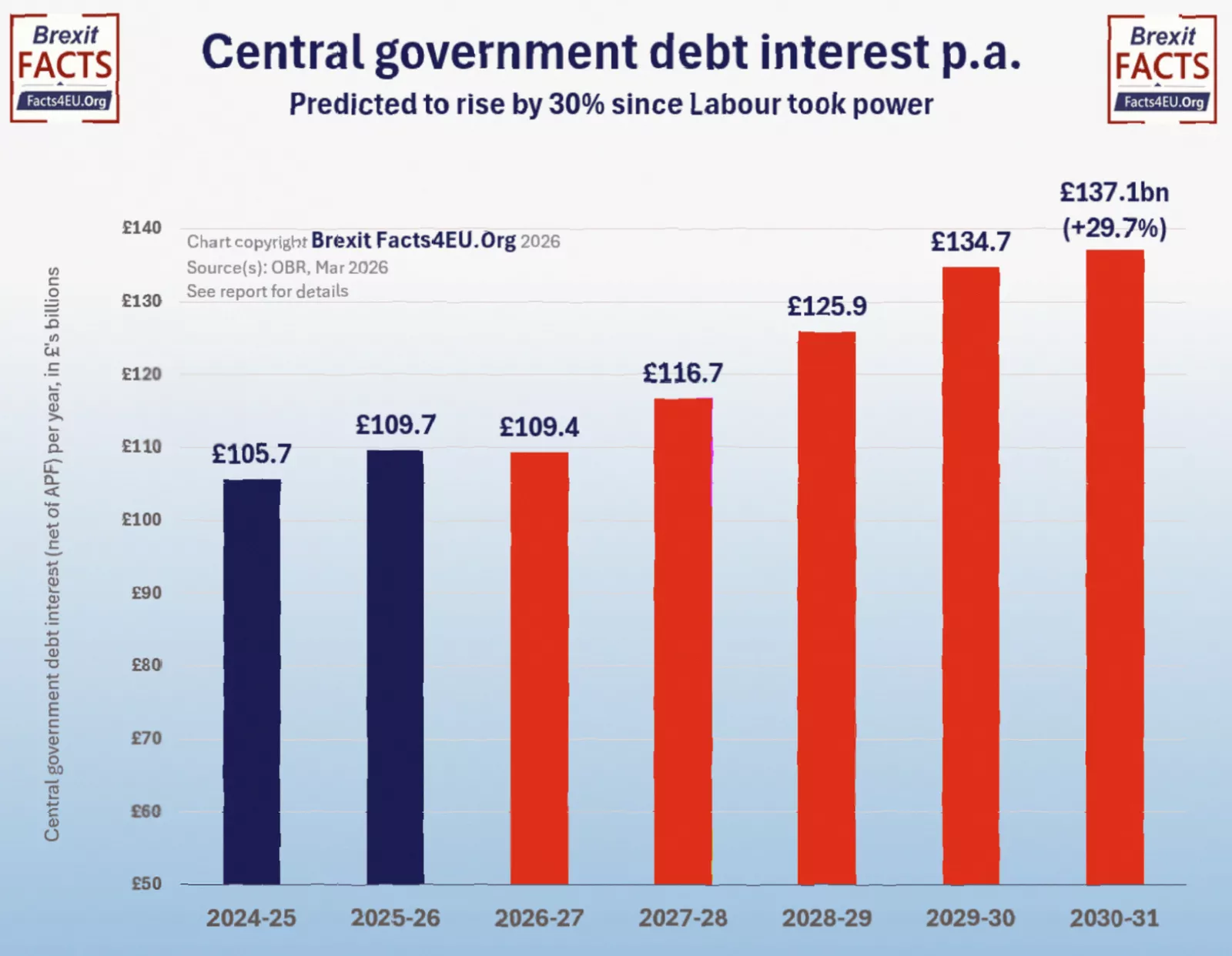

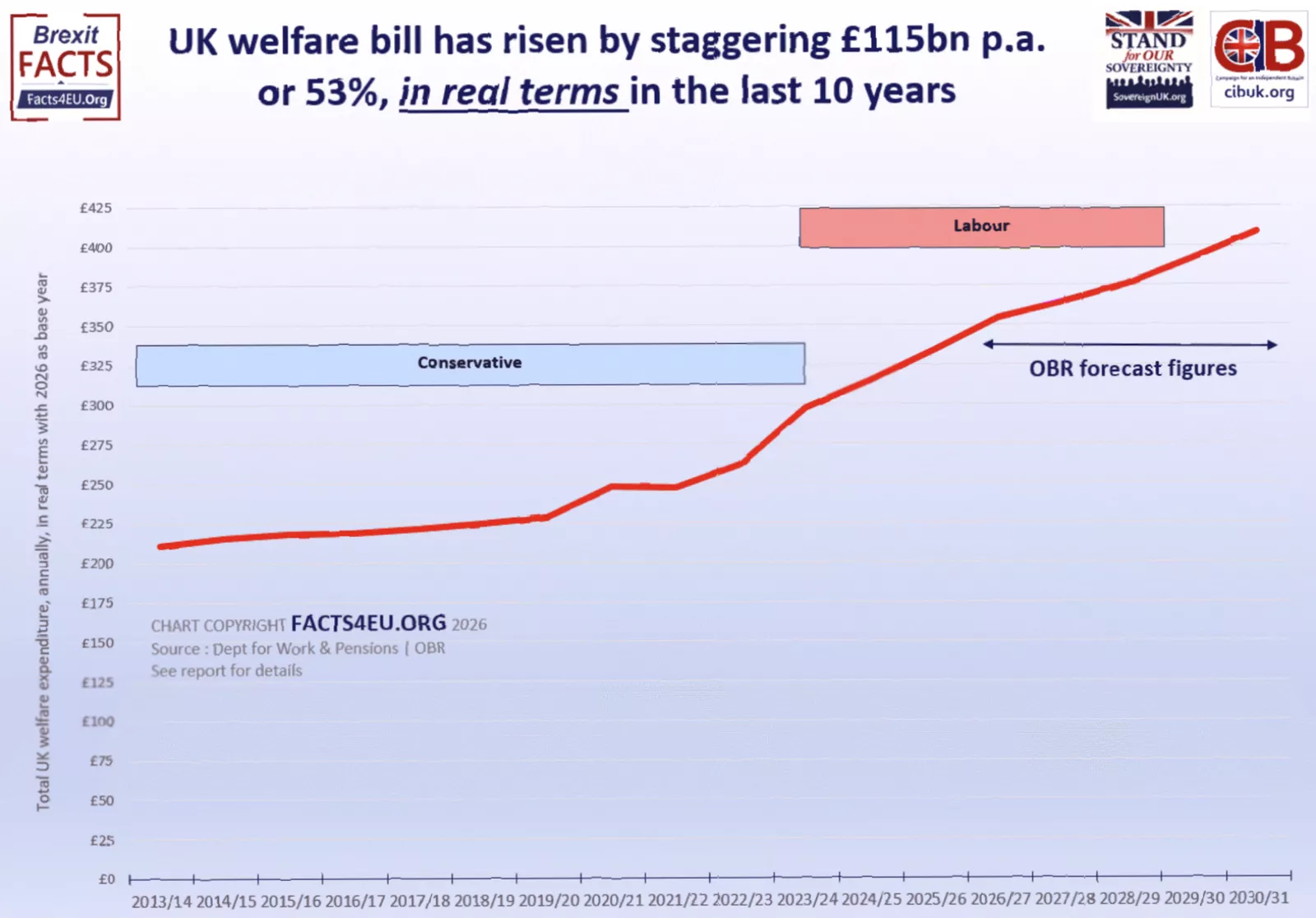

The cost of government borrowing has been much higher throughout 2025 and into 2026 than it was during the much-maligned premiership of Liz Truss, according to data cited in the original article. The Office for Budget Responsibility (OBR) has forecast that welfare spending – already rising sharply – will climb to more than £400bn by 2030/31, just five years from now. The research briefing gives more precise figures: the OBR projects an increase of £73.2bn over the next five years to £406.2bn. Disability benefits spending alone is forecast to rise from £39.1bn in 2023-24 to £58.1bn in 2028-29, while Universal Credit spending is expected to reach £88.1bn in 2028-29.

The original article argues that it seems improbable Miliband would reduce benefit spending or any public expenditure, and that bond markets will react fast, pushing up already-high debt interest payments. Spending on central government debt interest has been rising, and the OBR has published projections for the next five years. Any further borrowing to fund spending would be unsustainable given current poor economic growth, the article warned, and would need to be borrowed at ever-increasing rates, further adding to the annual bill. If taxes do not rise, markets will respond even more strongly.

The youth unemployment crisis adds another layer of economic strain. The original article cites a report by the Resolution Foundation, which found the rate of 18- to 24-year-olds not in education, employment or training (NEETs) was the third highest in Europe, after Italy and Lithuania, among analysed OECD countries. The research briefing provides updated figures: in October–December 2025, the NEET rate for 16- to 24-year-olds was 12.8% (957,000 individuals), and for 18- to 24-year-olds it was 15.2%. The Resolution Foundation identified a “quartet of causes”: rising ill-health among young people, weak vocational education, a hands-off benefits system, and a deteriorating jobs market. The number of 18- to 24-year-olds on benefits with no requirement to engage with the Department for Work and Pensions has increased from 160,000 to 300,000 since 2019. Only 22% of young people in the UK are in vocational education, compared with 35% in the Netherlands, Denmark and Germany. The Centre for Social Justice warned of a “toxic cocktail” of rising employment taxes, perverse incentives to claim benefits, and a broken migration system, reporting that in July–September 2025 there were 946,000 NEETs aged 16–24 – 196,000 higher than in 2019.

Lord Redwood, in comments carried by the original article, linked these trends directly to Miliband’s energy policies, arguing that “extreme green policies lead to the rolling collapse of petro-chemicals, plastics, ceramics, fibreglass, steel and many other energy using businesses. Worklessness soars and young people are left without jobs.” He predicted that if Miliband gains more influence after “bad election results for Sir Keir Starmer”, the country should expect more spending and borrowing, with Miliband seeking to spend more on his “green dreams in the vain hope there can be more green jobs.”

Miliband’s own policy record is anchored in his long-standing commitment to net zero. He was instrumental in steering the Climate Change Act through Parliament nearly 20 years ago, and the UK now has legally binding targets to reach net zero by 2050, with interim milestones of an 81% reduction by 2035 (announced at COP29 in 2024) and an 87% reduction by 2040 (the Seventh Carbon Budget). When Friends of the Earth and Greenpeace UK scored the party manifestos, Labour scored 20.5 out of 40 for its green plans – four times higher than the Conservatives but lower than the Green Party and Liberal Democrats. Miliband’s potential leadership would also see him operate alongside Chancellor Rachel Reeves, who was appointed the first woman to hold the office in July 2024 and has described her economic approach as “modern supply-side economics,” focused on infrastructure, education and labour supply while rejecting tax cuts and deregulation – a philosophy inspired by Joe Biden’s Inflation Reduction Act. Her first budget in October 2024 introduced the largest tax rises since March 1993, and she has pledged “iron discipline” over public finances. Yet the original article and the research briefing both point to fundamental disagreements between Miliband and Reeves over North Sea development, with the Energy Secretary’s refusal to countenance new oil and gas licences directly clashing with the Chancellor’s need for tax revenues and domestic energy supply to stabilise bills and public finances.

The collapse of oil refineries, the rising welfare and debt interest bills, the stagnation of youth employment, and the exposure of UK households to global energy price shocks all point to a stark choice, as Lord Redwood framed it: “The last thing we need is Mr Miliband as PM or Chancellor.”