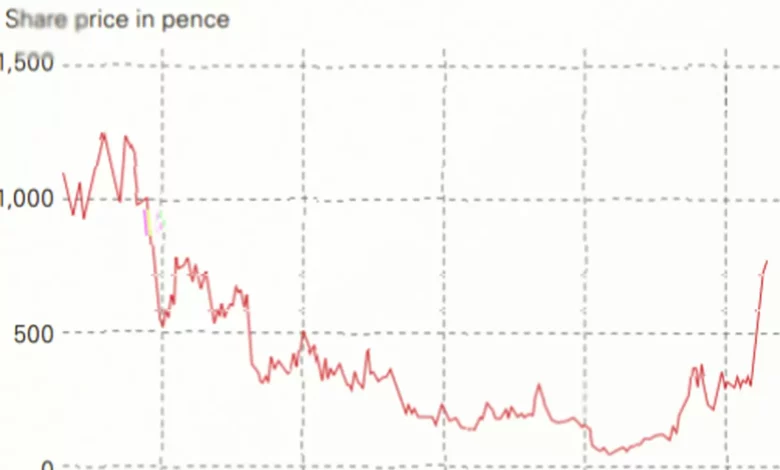

Ceres Power Holdings (LSE: CWR) has seen its shares surge 240% year-to-date, riding a wave of investor enthusiasm fuelled by the artificial intelligence boom. Over the past 12 months, the stock has climbed 850%, yet it remains roughly 50% below its ten-year high from February 2021. The UK-based developer of solid oxide fuel cells and hydrogen-power technologies, once overlooked because of high costs and low demand, is now at the centre of an energy arms race driven by the insatiable electricity needs of AI data centres.

The scale of the demand is staggering. Electricity consumption from data centres rose by 17% in 2025, and the average newbuild data centre is expected to require almost 110 megawatts (MW) of power by 2030, up from roughly 47MW in 2025, according to S&P Global. Globally, data centres could consume 1,000 terawatt-hours of electricity by 2023, double the level from 2030. Research from Gartner indicates that AI-optimised servers will account for 44% of data centre power consumption by 2030, while the International Energy Agency projects that power use from AI-focused data centres could triple by the end of the decade. In the UK alone, electricity demand from data centres is forecast to grow more than fivefold by 2030, reaching 26.2 terawatt-hours and representing 8.8% of total UK electricity demand. National Grid has warned of a sixfold increase in demand over the next ten years. A single training run of GPT-4 is estimated to consume roughly 50 gigawatt-hours, equivalent to the annual energy use of 40,000 U.S. households. The cumulative cost of meeting this demand could exceed $900 billion by 2050, analysts project.

The scramble for on-site power

Grid capacity constraints are pushing operators to seek their own power sources. In the United States, data centres are expected to require nearly three times as much grid power by 2030 compared with 2025, spurring a race for alternative supply. A landmark agreement in November 2024 between US utility American Electric Power and Bloom Energy, a competitor to Ceres, underlined the opportunity: the deal covers 1 gigawatt (GW) of solid-oxide fuel-cell products designed to plug directly into AI data centres. These fuel cells can run on natural gas, biogas or hydrogen blends and, crucially, can be delivered and turned on in months rather than years. Data centre operator EdgeCloudLink claims it can build and run a facility within nine months, partly because fuel cells eliminate reliance on power utilities.

Ceres Power now hopes to capture a slice of this market with its next-generation Endura technology, a solid-oxide stack platform that can operate on both natural gas and hydrogen. The core innovation is a ceramic electrolyte that converts fuels into electricity, and Ceres says its system does so more efficiently than rivals. At scale, manufacturing costs are expected to be one-third lower than competing technologies, according to the company, and the output matches the electrical requirements and standards of modern data centres, including high-voltage DC architectures up to 800V. Analysts at Berenberg describe the platform as a “gamechanger” that will allow Ceres to monetise its research and development into a scalable product. Peel Hunt, however, views it as little more than a “branding exercise” that repackages existing technology.

Licensing model and revenue potential

Ceres has moved away from a capital-intensive manufacturing model to an asset-light licensing approach, generating royalty revenue by granting partners the right to produce its technology. The company has set a goal of securing at least one new manufacturing licence agreement per year. That target appears modest against the backdrop of a 22GW market opportunity it has identified by 2030, driven by demand from industry and data centres, particularly in Asia and the Americas.

The financial implications of a single large licence are significant. According to Berenberg, if one partner scaled up to 1GW of production using Endura, it could generate between £50 million and £100 million in annual royalty revenue. At current sector valuation multiples, that would translate into $1 billion of shareholder value. Compared with Ceres’s current market capitalisation of roughly £1.4 billion, the potential upside explains the rush of investors into the stock. (As of May 2026, the market cap had risen to £1.57 billion.)

Executing on that promise is far from certain. Ceres’s revenue has been erratic – it did not grow over the five years before 2025. Revenue for the year ended 31 December 2025 was £51.9 million, a 132% increase from the previous year, but the company remains loss-making. Earnings before interest, tax, depreciation and amortisation (EBITDA) is projected to turn positive only in 2028, at £7.8 million. Peel Hunt has cut its 2026 revenue estimate to around £45 million, excluding new business, and downgraded the stock to “Sell” in April 2026, citing an “overly optimistic” growth outlook. The shares trade at 17.5 times forward sales, a multiple that leaves little room for error if sales disappoint.

Partnerships and cash runway

Ceres has nevertheless been building a network of collaborations. In March 2026 it announced a partnership with Centrica, the owner of British Gas, and in April 2026 it joined forces with Centrica and Delta Electronics, a manufacturing licensee, to target off-grid energy generation for data centres and industrial sites. The plan is to deploy a demonstration site within 12 months and scale capacity over three to five years, offering customers “competitively priced, on-site power generation, significantly reducing exposure to wholesale electricity market volatility and grid capacity constraints”. Other partnerships signed in 2025 are expected to start delivering results in 2026, including agreements with Shell in India, Doosan in South Korea, and Weichai in China. A joint venture with Bosch ended in February 2025.

Financially, the company is burning cash – it consumed £20 million in 2025 – but it has £83 million in the bank at the end of the year, enough to sustain operations for roughly three more years until break-even. Costs are expected to fall by about 20% in 2026.

Spun out from Imperial College London in 2001 and listed on the London Stock Exchange in 2004, Ceres has won the Royal Academy of Engineering’s MacRobert Award and the Queen’s Award for Enterprise. Its technology now sits at the intersection of a massive structural shift: the UK alone needs an additional 50GW of electric supply to meet the data centre projects in its pipeline. For Ceres, even a relatively small order could transform its fortunes – but the gap between promise and profit remains wide.