Global financial markets have been thrown into turmoil and the world’s energy supply plunged into crisis after a dramatic escalation in the Middle East conflict triggered the most severe oil price shock in four years. The price of Brent crude surged past $100 a barrel and at one point neared $120, its biggest daily leap since the depths of the Covid-19 pandemic, following a weekend of intensified hostilities that directly targeted the region’s energy infrastructure.

Geopolitical Flashpoint Sparks Energy Crisis

The immediate catalyst was a series of strikes on at least five energy sites in and around Tehran, described as causing “apocalyptic” scenes in the Iranian capital. This marked a significant tactical shift, with analysts noting both sides had begun targeting oil infrastructure after largely avoiding it in the conflict’s early days. The strategic chokepoint of the Strait of Hormuz, a conduit for about 20% of the world’s oil and 27% of global seaborne crude, has been effectively closed, severing a critical artery for global energy trade.

The closure has forced drastic production cuts across the Gulf. Iraq’s oil-dependent economy has been dealt a severe blow, with output from its main southern fields falling by 70% to just 1.3 million barrels per day, as storage fills up with nowhere to export. Kuwait’s national oil company announced a “precautionary” reduction in production and refining and declared force majeure on exports, while Qatar has done the same for its liquefied natural gas shipments. Qatar’s Energy Minister has warned that all Gulf producers could be forced to halt energy exports within weeks if the conflict persists.

Adding to the sense of a protracted conflict was the confirmation of Mojtaba Khamenei, the second son of the late Ayatollah Ali Khamenei, as Iran’s new Supreme Leader. Ipek Ozkardeskaya, senior analyst at Swissquote, stated this choice “did not please the US at all” and suggests Iran will not back down, pointing to “a potentially prolonged war in the Middle East – which is home to about 50% of global oil reserves.” US President Donald Trump responded by saying he was “not happy” with the selection, insisting the US must be involved in choosing Iran’s leader.

Markets Plunge as Inflation Fears Return

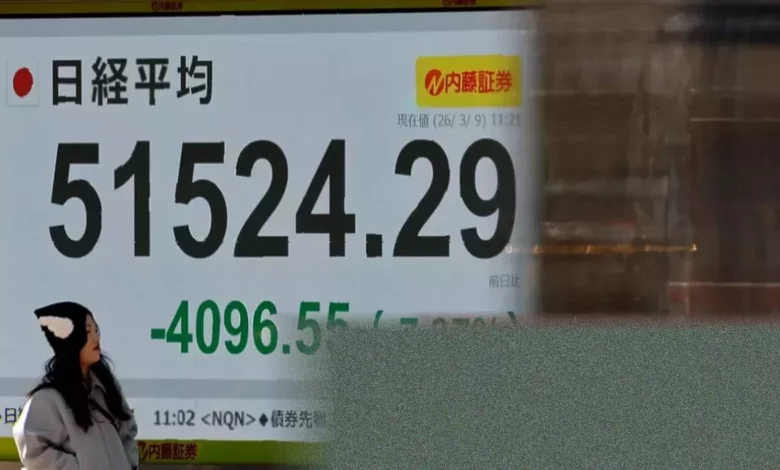

The reaction across global financial markets was immediate and brutal. In Asia, Japan’s Nikkei plunged almost 5%, South Korea’s Kospi shed 6.5%, and Australia’s S&P/ASX 200 dropped 2.85%. The sell-off continued in Europe, where Germany’s DAX fell 2.5%, France’s CAC 40 lost 2.4%, and Spain’s IBEX dropped 3.1%. The pan-European Stoxx 600 sank 2% to its lowest level since December.

In London, the FTSE 100 index tumbled 1.75%, wiping out most of its gains for the year. Sectors exposed to higher costs and reduced consumer spending were hammered. Airline shares slid sharply, with IAG (parent of British Airways) down 4.3%, Lufthansa off 4.6%, and Air France falling 5.1%. Mining stocks like Anglo American and Antofagasta fell over 5%, while Rolls-Royce, whose jet engine business is sensitive to air travel demand, dropped 5%. The only significant risers were the oil majors Shell and BP, which gained from the surging crude price.

The turmoil spread to bond markets, where fears of a new inflationary surge drove prices down and yields up. The yield on the benchmark 10-year UK government bond jumped sharply. “The UK is paying more for natural gas than our European neighbors, so it is natural that our bond market sell off could be worse,” noted Kathleen Brooks, research director at XTB. The pound also slid against the US dollar as investors sought the traditional safe-haven currency, which is further bolstered by America’s status as a net energy exporter.

European natural gas prices, already volatile, surged in tandem with oil. The UK month-ahead gas price jumped 19%, while the continental European benchmark rose 16%, adding to recent spikes as high as 70% in recent days.

Policy Makers Scramble to Respond

Faced with a potential global economic shock, policymakers began discussing coordinated action. According to the Financial Times, G7 finance ministers are to hold a call with the International Energy Agency (IEA) to discuss a potential joint release of emergency oil reserves from their strategic stockpiles. Some US officials reportedly believe a release of 300-400 million barrels—a significant portion of the 1.2 billion barrel reserve—would be appropriate. The IEA system, established after the 1974 Arab oil embargo, has been activated only five times before, most recently after Russia’s invasion of Ukraine.

The shock has also upended expectations for monetary policy. In the UK, any lingering hope of a Bank of England interest rate cut this month has been crushed; money markets now indicate a 99% probability rates will be held steady on 19 March. Before the escalation, a cut had been an 80% chance. Looking further ahead, traders are now pricing in a greater likelihood of a rate increase than a cut this year.

National governments are also preparing measures. Japan’s Prime Minister Sanae Takaichi told parliament the government was considering steps, potentially funded from reserves, to curb gasoline prices and cushion the economic blow from rising fuel costs. Japan recently approved a $32 billion emergency package to counter rising energy and food costs.

Broader Economic Fallout and Human Cost

Beyond the markets, analysts warn of severe consequences for global growth and inequality. The IMF has estimated that every sustained 10% rise in oil prices lifts inflation by 0.4% and reduces global economic growth by 0.15%. Fitch Ratings has warned that emerging market economies, particularly net fossil fuel importers like India, face challenges through energy imports, remittances, and exchange rate pressures.

Research highlighted by the original wire report underscores that the pain will not be evenly shared. Economists from the University of Massachusetts Amherst have identified energy as a commodity with a “disproportionate capacity to increase inequality when its prices rise.” A study of the 2022 oil price surge in the US found that 50% of the windfall benefits accrued to the wealthiest 1% of individuals via the stock market, while the bottom 50% received only 1%.

Countries that are net importers of oil, such as the UK, are “unambiguously losers from higher energy prices.” President Trump, however, framed the costs differently, posting on his Truth Social platform that the “short term oil price… is a very small price to pay for U.S.A., and World, Safety and Peace,” predicting a rapid drop once the “Iran nuclear threat is over.”

With the Strait of Hormuz closed, key producers issuing force majeure, and diplomatic tensions heightened by Iran’s new leadership, the crisis shows little sign of abating. As Jim Reid, market strategist at Deutsche Bank, observed, the targeting of oil infrastructure over the weekend represents a clear escalation, leaving investors and governments bracing for a prolonged period of energy-led economic turbulence.