Over 50 of the world’s poorest nations are now confronting the biggest debt crisis in history, as interest payments swallow vast portions of public budgets that ought to be spent on hospitals, schools and climate resilience. The scale of the crisis is staggering: 25 African countries are spending more on interest owed on foreign debts than on education, a direct trade-off between corporate profits and teaching the next generation. By the end of 2023, developing economies collectively owed $29 trillion in public debt – nearly 30 per cent of the global total – and in Africa alone external debt more than doubled from $323 billion in 2013 to $685 billion in 2023.

The scale of the crisis

The burden on low- and middle-income countries is intensifying. The United Nations reports that 19 developing countries spend more on debt interest than on education, and 45 spend more on interest than on health. Globally, 48 developing nations – home to roughly 3.3 billion people – allocate more to interest payments alone than to either education or health. Between 2010 and 2023, spending on interest payments in developing countries rose by 73 per cent, while health and education spending grew by only 58 per cent and 38 per cent respectively. In some cases, debt servicing consumes as much as 60 per cent of education expenditure.

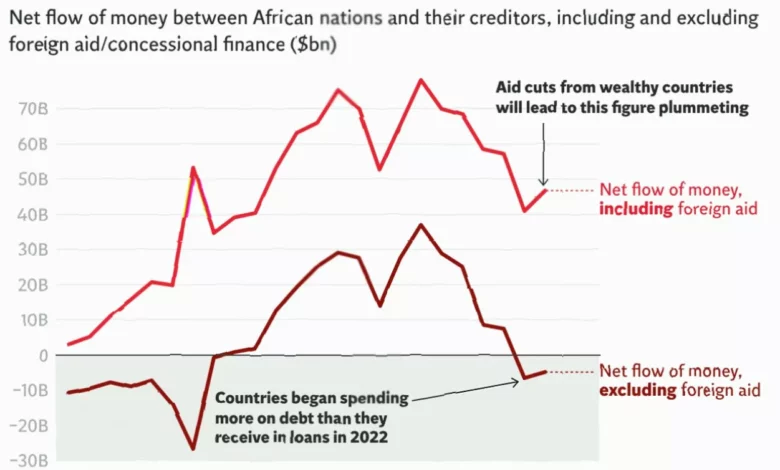

By 2024, African governments committed $104 billion to debt servicing, with $47 billion going directly to private creditors. In 34 nations across the continent, debt payments outstripped combined spending on health care and education. The situation is so dire that in 2023, 26 countries experienced net negative financial transfers – meaning they paid out more to creditors than they received in new financing – totalling $48 billion. Projections for 2025 suggest this could hit 44 countries, with transfers exceeding $100 billion, effectively forcing developing nations to subsidise global capital markets.

This crisis did not emerge overnight. The Heavily Indebted Poor Countries (HIPC) initiative, launched in 1996, cancelled around $99 billion in debt for 36 countries and produced measurable gains – primary school completion rates in benefiting nations rose from 45 per cent to 66 per cent as savings were redirected into public services. But the system was not fully fixed, and a new debt crisis has developed, this time driven predominantly by private lenders rather than governments.

How UK law enables the crisis

At the heart of the current predicament is the role of English law. An estimated 90 per cent of debt contracts between private creditors and countries facing debt crises are governed by English law, making UK courts the primary venue for enforcing sovereign debt. This legal architecture gives profitable private lenders – banks, asset managers and hedge funds, many based in the UK – an extraordinary weapon: the ability to sue debt-distressed nations in British courts for the full face value of debt they may have bought at a steep discount.

These entities, often described as vulture funds, acquire the sovereign debt of economically struggling countries for pennies on the pound and then pursue legal action to recover the nominal value plus accumulated interest. Unlike official lenders such as the UK government, private creditors can impose harsher terms, including huge interest rates, and frequently hold out from restructuring debts on terms comparable to those offered by governments and multilateral institutions. The result is eye-watering profits extracted from the world’s poorest countries even as they are battered by conflict, extreme weather and global economic shocks.

There is no robust international process to compel private creditors to come to the negotiating table on debt relief. Regulation exists in the UK to protect individuals from payday loan sharks, and businesses have access to bankruptcy courts that make impartial rulings on debt renegotiation. But sovereign nations have no equivalent. As Indermit Gill, Chief Economist at the World Bank, has put it: “Sovereign borrowers deserve at least some of the protections that are routinely afforded to debt-strapped businesses and individuals under national bankruptcy laws.”

The threat of litigation is not theoretical. In February 2026, a group of bondholders announced their intention to bring legal action against Ethiopia in UK courts. They acted after official creditors – co-chaired by China and France – rejected a draft restructuring agreement on the grounds that it did not meet the “Comparability of Treatment” principle under the G20’s debt restructuring initiative. Analysis showed that bondholders would have been paid 28 per cent more than government lenders under the rejected offer, at the expense of taxpayers in official creditor countries like the UK. The bondholders stated they were left with “no other option but to take legal action.”

Other nations have operated under the shadow of similar threats. War-torn Ukraine faced the prospect of legal action from private creditors seeking better terms on their holdings, using the threat of UK court proceedings as leverage for private profit. The “holdout problem” – creditors who refuse to join restructuring plans in the hope of extracting more than their fair share – is well documented. Collective Action Clauses in some debt contracts have proved insufficient to prevent it.

The UK passed the Debt Relief (Developing Countries) Act in 2010 to curb the worst excesses of vulture funds, making it permanent the following year. That legislation prevented creditors from suing for more than they would have received under HIPC-era restructurings. But the landscape has shifted dramatically since then: the HIPC initiative is effectively closed, and the G20’s Common Framework for Debt Treatments – designed to restructure unsustainable debts – has been widely criticised as ineffective, with private creditors largely refusing to engage since 2020.

A proposed legislative solution

In November 2024, Labour MP Bambos Charalambous introduced a new Debt Relief Bill to update and strengthen the 2010 Act. The Bill would cap the amount that creditors who hold out on negotiations can claim, and would prohibit lawsuits against debt-stricken countries while restructuring processes are under way. It is designed to apply to current debt treatment initiatives, including the G20’s Common Framework. The Bill passed its first reading on 13 November 2024 and was scheduled for its second reading in spring 2025.

The need for action has only grown since the Bill was first tabled. In 2024, detractors argued the legislation was unnecessary because no countries had recently been sued in UK courts. The Ethiopia case has now overturned that claim. Meanwhile, voices calling for reform continue to multiply. The African Union, via its Lomé Declaration on Africa’s Debt – adopted at its first debt conference in Lomé, Togo, in May 2025 – called for a unified African position on debt governance, including revisions to the G20 Common Framework, greater transparency, suspension of debt service during negotiations, and recognition of debt cancellation as an instrument of economic justice.

In June 2025, the Vatican’s “Jubilee Report” – chaired by Nobel laureate Joseph Stiglitz – recommended a “legislated cap on recoveries by private creditors” and an international bankruptcy system for sovereign nations. It highlighted that 3.3 billion people live in countries that spend more on interest payments than on health, and 2.1 billion live in countries that spend more on interest than on education. High commissioners, faith leaders, expert economists and academics have all pointed to legislation in the UK as a critical lever. The UK government has said it is keeping potential legislation under review, but the longer action is delayed, the deeper countries like South Sudan spiral into crisis – at the expense of health and education for their citizens, and at a time when global aid budgets are being slashed.