The latest snapshot of the cost-of-living crisis is due this week, with economists expecting the headline rate of inflation to have remained stubbornly high in February, held up by rising air fares and clothing prices even as fuel costs fell.

Official Consumer Prices Index (CPI) figures for February 2026 will be published on Wednesday. Analysts are broadly predicting the rate will have either held steady or dipped only slightly from the 3.0% recorded in January. Economists at Deutsche Bank and Pantheon Macroeconomics anticipate it holding at 3%, while Barclays forecasts a dip to 2.9%. Edward Allenby, senior economist at Oxford Economics, expects a fall to 2.8%.

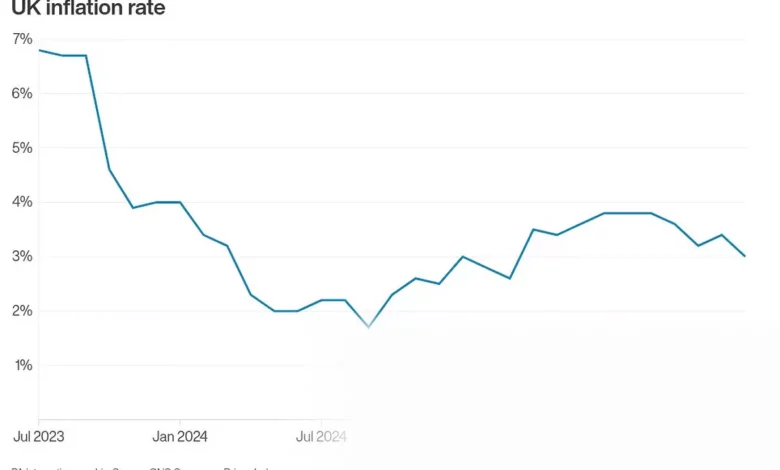

January’s figure of 3.0% itself represented a drop from 3.4% in December 2025 and was the lowest annual rate since March of the previous year. That easing was driven by softer rises in transport and food costs, according to the Office for National Statistics data. Core inflation, which strips out volatile energy, food, alcohol, and tobacco prices, also fell to 3.1% in January—the lowest reading since September 2021.

Geopolitical Shock Reverses the Tide

However, this fragile progress towards the Bank of England’s 2% target is now under severe threat from a sharp geopolitical twist. Experts warn that the escalating conflict in the Middle East is set to send energy bills soaring, creating a new and significant “hump” in the UK’s inflation profile over the coming summer.

The Bank of England has already ripped up its own projections in response. On Thursday, it stated that recent surges in wholesale energy costs would delay inflation’s return to target. It now expects inflation to be around 3% in the second quarter of this year, a sharp revision from the 2.1% it forecast just last February, and anticipates it could rise to around 3.5% by the third quarter.

“The UK’s disinflation story will take another twist on its (eventual) way down to target,” warned Sanjay Raja, Deutsche Bank’s chief UK economist. “The bad news? Higher energy prices appear poised to lift CPI meaningfully over the summer.”

Energy Market Turmoil Hits Home

The scale of the shock to global energy markets is dramatic. Since US-Israel attacks on Iran in late February, wholesale gas prices have surged by 67% and oil by 35%. By mid-March, Brent crude oil had reached $115 a barrel due to disruptions in the critical Strait of Hormuz, while UK gas futures for this summer were trading 91% higher than a month prior.

This wholesale turmoil translates directly into higher household costs. The UK generates around 30% of its electricity from gas-fired power plants, making it acutely vulnerable. Analysts at Cornwall Insight now predict the Ofgem energy price cap for July to September will rise to approximately £1,973—a jump of around £332, or 20%, on the April cap. Another major supplier, E.ON Next, forecasts the July cap at £1,849.

“Under our updated assumptions, we now anticipate a much sharper rise in petrol prices, while higher wholesale gas prices cause a 19 per cent increase in the Ofgem energy price cap in July,” said Edward Allenby of Oxford Economics, who now expects CPI inflation to exceed 4% in the second half of the year. Pantheon Macroeconomics also agrees CPI could reach 4% later this year if the gas price spike is sustained.

Motorists face a double squeeze. Petrol prices are already rising, with average unleaded around 136p per litre in early March. Furthermore, the government confirmed in its Spring Statement that the temporary 5p fuel duty relief will end on 31 August. From September, duty will rise by 1p per litre, with the remaining 4p increase phased in before March 2027.

Broader Economic Repercussions Loom

The Bank of England’s Monetary Policy Committee (MPC), which voted unanimously to hold the Bank Rate at 3.75% on 18 March, cited the conflict’s impact as a key concern. It is now alert to the risk of “second-round effects,” where sustained higher energy costs bleed into domestic wage demands and price-setting, creating longer-lasting inflationary pressure.

This new uncertainty has clouded the outlook for interest rates, with some analysts, including those at Deutsche Bank, suggesting further rate hikes could be necessary if energy prices remain elevated. Prior to the conflict, cuts had been widely anticipated.

The shock is also affecting broader economic forecasts. Deutsche Bank has revised down its UK GDP growth forecasts to 1.3% for 2025 and 1.4% for 2026, citing weaker private sector demand and rising costs. It expects wage growth to slow gradually and unemployment to peak at 4.6% by late spring 2025.

While the Office for Budget Responsibility (OBR) has forecast inflation to be 2.3% across 2026, meeting the 2% target by 2027, the central bank has stressed the situation is volatile. The coming six weeks are likely to be critical in determining the scale of the disruption and its full impact on household finances, meaning the hoped-for respite from high prices has been postponed indefinitely.