Rachel Reeves pension tax raid damages more than officials first revealed, millions impacted

Millions of workers may reduce pension savings due to new tax rules, with official projections suggesting more than 2.8 million employees are expected to cut their retirement contributions once restrictions on salary sacrifice come into force in April 2029.

The figure, obtained by former pensions minister Steve Webb through a Freedom of Information request to HM Revenue and Customs, was initially withheld by the tax authority on the grounds that it related to policy development. Following an appeal, HMRC released additional data in May. The total affected is sometimes cited as nearly three million, with HMRC estimating 2.9 million workers will scale back their pension saving.

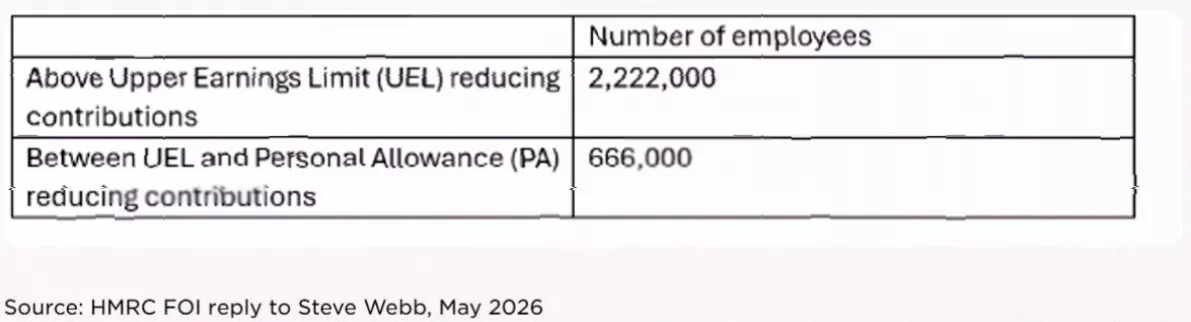

Of those projected to reduce contributions, approximately 2.2 million are higher‑rate taxpayers earning above the Upper Earnings Limit of £50,270 a year. A further 666,000 are basic‑rate taxpayers, representing nearly one in four of the total affected workforce.

How the salary sacrifice cap works

Salary sacrifice allows employees to give up part of their gross salary in exchange for an equivalent employer pension contribution. Because the sacrificed salary is no longer counted as earnings, the worker pays less income tax and lower employee National Insurance contributions, while the employer also saves on employer National Insurance. The arrangement has been widely used, particularly by higher earners, to boost pension saving while reducing immediate tax liabilities.

From April 2029, the Treasury will impose a £2,000 annual cap on the amount of employee pension contributions that can be made via salary sacrifice while remaining exempt from both employee and employer National Insurance. Contributions above that limit will attract National Insurance charges, eliminating the tax advantage that made the arrangement attractive.

The policy is expected to raise substantial revenue for the government. The Office for Budget Responsibility projected the measure would bring in £2.6 billion a year by the early 2030s. Other official estimates put the figure at £4.8 billion in 2029‑30 and £2.5 billion in 2030‑31, or around £4 billion a year in the first year of operation.

Impact across income groups

Analysis from the Institute for Fiscal Studies shows that salary sacrifice arrangements are heavily concentrated among the highest earners. Around 48% of employees in the top 10% of earners make salary sacrifice pension contributions above £2,000, compared with less than 1% in the lowest‑earning fifth. Consequently, the majority of the additional National Insurance liability will fall on higher‑income employees and their employers.

Yet the OBR’s assessment suggests that lower earners will make the most substantial reductions to their pension contributions. The increase in National Insurance costs may prompt them to save less in order to protect their take‑home pay. The OBR warned that the behavioural impact of the new cap on pension saving is “highly uncertain”.

The private sector will be disproportionately affected, according to the IFS. Around 18% of private sector employees use salary sacrifice above the £2,000 threshold, compared with 7% in the public sector. Industries such as finance, insurance, information and communication are particularly exposed.

The policy also increases employer National Insurance costs. The IFS anticipates that employers will pass on much of this cost to employees through lower wages. Some employers may abandon salary sacrifice schemes entirely, moving staff to a “relief at source” system, which could reduce take‑home pay even for workers who do not breach the cap.

The impact on take‑home pay is not always directly correlated with income level. Because of the way National Insurance thresholds operate, someone earning around £50,000 could see a larger reduction than a colleague earning £55,000.

Criticism and government defence

Steve Webb, partner at LCP and a former pensions minister, condemned the policy as “far more damaging than had previously been admitted”. He said: “The Government has presented the changes to salary sacrifice for pensions as being a relatively painless way of cracking down on a tax break mostly enjoyed by the well off. But these figures show that the effects of the policy will be far more damaging than had previously been admitted.”

He added: “It is hardly ‘joined‑up government’ to be stressing the need for more pension saving one day and then implementing a policy that will reduce the pension savings of millions the next.”

The criticism comes at a time when the government‑backed Pensions Commission has estimated that roughly 15 million working‑age people are already failing to save enough for retirement — a figure that could rise to 19 million without intervention. Recent updates to Retirement Living Standards show that a “comfortable” retirement for a single person costs £45,400 a year, and £62,700 for a couple. Only 9% of the working population is on track to achieve that level.

A Treasury spokesperson defended the reforms, saying: “High earners piled in huge bonuses through salary sacrifice without paying a penny in tax – a taxpayer funded perk largely benefitting the better off. Our fair reforms protect 95% of workers earning under £30,000 using salary sacrifice, and as IFS analysis shows, over three quarters of under 30s will be unaffected.”

In March, the House of Commons overturned House of Lords amendments that had sought to raise the cap from £2,000 to £5,000 and to exclude basic‑rate taxpayers from the measure.

The IFS has criticised the reform for creating “another new arbitrary line in the tax system” without addressing fundamental asymmetries in pension taxation.